EU Tax Dispute Resolution:

The EU Tax Arbitration Convention

2001 Dr Jean-Philippe Chetcuti. All Rights Reserved.

In this paper, the Convention is explained from various points of view. First of all, the troublesome process of its adoption is traced from a historical perspective, starting from the earliest debates on the need for such a measure. Then follow detailed explanations of the scope and the subject matter of the Convention and its workings.

Table of Contents

1. The process of the adoption of the Convention

Following up its Communication to the Council of November 1973 on multinational undertakings, the Commission stressed in its 1975 action programme that it would continue its work with a view to presenting a proposal on the elimination of double taxation which can result from adjustments made to profits by a MS.

1.1. A fair complement to the Mutual Assistance Directive

This proposal for a directive was made on 29 November 1976 when the Commission presented a draft Council Directive on an arbitration scheme to settle double taxation disputes to complement its proposal for a directive on mutual assistance in taxation measures. In its explanatory memorandum, the Commission stressed the close link which this proposal maintained with the Mutual Assistance Directive. The Commission acknowledged that the introduction of a system for the exchange of information between the tax authorities could potentially increase the number of instances of double taxation, particularly in the field of transfer pricing. Thus, the Commission felt that the Arbitration Directive should be adopted simultaneously with the Mutual Assistance Directive to ensure for community taxpayers a remedy for instances of double taxation ensuing from overlapping assessments of the same income in more than one jurisdiction.

In a session held in Brussels on 26 and 27 October 1977, the opinion submitted by the Economic and Social Committee of the European Community was generally favourable and the (nine) MSs were in agreement on the principle underlying this draft directive. On 14 June 1977, the European Parliament submitted its position and the EC Council commenced its deliberations in 1978.

1.2. Causes of delay

1.2.1. The binding nature of awards and the jurisdiction of the ECJ

The adoption of the proposed directive was held-up, inter alia, because the Financial Committee of the Council disagreed on whether the findings of the Arbitration Commission should be binding and on the competence of the ECJ. The application or interpretation of a convention cannot be submitted to the jurisdiction of the ECJ and therefore, the legal protection of companies would be limited. At the most they would be able to summon their own tax authorities before the national court if they think that the Convention has not been correctly applied. Neither can the European Commission take MSs to the ECJ where MSs are considered to be acting contrary to the provisions of the Convention, as in the case of a directive.

1.2.2. Legal form & legal basis

Moreover, the Council was of the opinion that the issue should be tackled by a multilateral convention based on Article 293 of the EC Treaty rather than by a directive. Under Article 293, MSs desire to eliminate double taxation must be met through negotiations between the independent MSs. These negotiations should eventually culminate in a multilateral convention.

At the initiative of the Netherlands, the proposed directive of 1976 was transformed into a convention. The draft convention prepared by the Dutch government was the final product then submitted by the Commission for adoption by all MSs.

1.2.3. Unwillingness of MSs to surrender fiscal sovereignty

From that point onwards, it took fourteen years to have the measure adopted. A possible difficulty which could have served to hold back the introduction of a mechanism for the elimination of double taxation resulting from transfer pricing adjustments was the typical unwillingness of the MSs to surrender such a fiscally sensitive area to the authority of a supranational entity. Evidence pointing to the probable reason for the dragging of feet on the issue is the careful terminology employed in the wording to the official title of the Convention in that it fails to include the term arbitration or arbitration procedure so as not to emphasise the supranational elements of an arbitral commission. Going back to the 1976 Arbitration Directive, the Explanatory Memorandum included in the Commissions proposal assured MSs that the suggested arbitral commissions by no means constitute supranational judicial bodies.

1.2.4. The package approach

The fact that the Mutual Assistance Directive was adopted on 19 December 1977 and amended on 6 December 1979, while the arbitration directive was delayed until 1990, was condemned by advisers claiming that, at least in the field of direct taxation, the European Community didnt protect the interests of taxpayers as much as the interests of the tax administrations. It has been argued that this demonstrates that measures originally intended to pass through Council as a package should be dealt with, and enacted by, the Council simultaneously.

On 17 January 1984, Mr Tugendhat, Commissioner for taxation, addressed a Communication to the Council treating fiscal measures aimed at the encouragement of co-operation between undertakings of different MSs. This Communication dealt with four proposals: EEIG Regulation, Merger Directive, Parent-subsidiary Directive and the Convention. At the time, the Commissioner stressed that it was only the outcome which mattered. Thus the Commission was ready to accommodate any requests to amend the said proposals as long as they resulted in the elimination of double taxation.

The Commission addressed another Communication to the Council on fiscal measures aimed at encouraging co-operation between undertakings of different MSs, and aspiring for the quick approval of the Merger and Parent-subsidiary Directives and the Arbitration Convention. However, agreement on these measures was only reached after another five years. Arguably, tying the Convention to the Merger and Parent-subsidiary Directives could have held up the process of its adoption; however, as the result demonstrates, the Commission has thus succeeded in seeing the adoption of all three measures together.

1.3. The breakthrough

On 23 July 1990, the Ministers of Finance of the twelve EC MSs agreed on a multilateral Convention on the Elimination of Double Taxation in Connection with the Adjustment of Profits of Associated Enterprises (hereinafter, Convention). France was the first State to deposit the instrument of ratification on 21 February 1992 while Portugal was the last State to deposit the instrument of ratification on 28 October 1994. Article 18 of the Convention states that entry into force would be on the first day of the third month following the depositing of the instrument of ratification by the last signatory State. Accordingly, the Convention came into effect on 1 January 1995, between Belgium, Denmark, Germany, Greece, Spain, France, Ireland, Italy, Luxembourg, the Netherlands, Portugal and the UK.

1.4. Accession, life span and possible termination

In 1995, the three new MSs, Finland, Austria and Sweden concluded a separate Treaty of accession to the Convention which would enter into force -between the ratifying States three months after at least one of the three new MSs and at least one of the old twelve MSs ratifies it. For MSs which would ratify later, it would enter into force three months after their ratification. The Accession Convention has resulted in minor adjustments to the terms of the main Convention (the taxes affected by the Convention, the definition of competent authorities and the notion of serious penalties in the acceding States).

The initial application period of five years expired as on 1 January, 2000. However, the Convention could be expressly extended by the Contracting States before 1 January 2000. In fact, the life span of the Convention was extended with an additional period of five years by Protocol on 25 May 1999. The Protocol is subject to ratification by all (now) fifteen MSs and it will not enter into force until the beginning of the third month following ratification by the last MS. On entry into force, the Protocol will give retrospective effect to the Convention as from 1 January, 2000.

The Convention is not in force at this point in time and, until the fifteenth MS finally ratifies the Protocol, MNGs of companies operating within the EU face a vacuum in their protection against double taxation. There also remains the possibility that not all MSs will ratify in which case the Protocol will never come into force. The Convention will in fact have been terminated as per 1 January 2000.

As Luk Hinnekens suggests, the time limit may result in timing problems. The Convention does not provide for procedures which will still be pending at the end of an unrenewed five-year term. It seems therefore, that such cases, if any, will have to be continued on the basis of domestic law or mutual agreement procedures. It is suggested that, for the time being, taxpayers can partially escape these obstacles by formally initiating domestic legal remedies and then withdrawing under the strict condition that the procedures of the Convention apply.

While under the original agreement from 1990, any extension required the unanimous consent from all MSs, it has now been agreed that the extension will occur automatically unless the MSs decide otherwise. This avoids the need for MSs actively agree on further extensions. The other option was that MSs agree that the Convention be extended indefinitely.

2. Transfer pricing practices, price-adjustment of cross-border dealings and resulting double taxation

The scenario which the Convention sets out to address is one of transfer pricing. This heading explains the practice of transfer pricing and how international double taxation arises therefrom.

2.1. Intercompany and intracompany dealings

The transfer of intermediate products and services among different companies forming part of the same group of companies is not uncommon and, given the group relationship existing between such companies, one can understand why such transfers do not occur at prices which would apply between two unrelated companies (arms length prices). Technically, the financial position of the group as a whole remains unaltered by, and is indifferent to, the pricing of intra-group transactions since with the flow of such goods or services within the group, the loss which one member company suffers as a result of such transfer-pricing is compensated by a corresponding profit ensuing in the hands of the other party to the transaction. In fact, this is so until the goods or services leave the group, in which event the profit or loss generated by a member of a group transacting with an unassociated company becomes the profit or loss of the whole group.

2.2. Reasons for transfer pricing

Fiscally, this principle of the neutrality of groups to intra-group transfer pricing does not apply to MNGs of companies. Due to differences in fiscal law between MSs, the pricing of intra-group transactions and resulting profits out of one national tax jurisdiction into another may have very significant consequences on the overall tax position of the group. There is a considerable potential for multinational companies to shift (whether artificially or otherwise) significant amounts of taxable profits to subsidiaries in jurisdictions with low or zero corporate tax rates, in order to avoid payment of taxation on profits or to attract lower tax rates. In practice, such tax saving structures of affiliates in tax haven countries are relatively easy to set up. For tax authorities, profit transfers translate into a decreased inflow of fiscal revenue into public coffers. For this reason, multinational companies with subsidiaries in lower tax jurisdictions are particularly susceptible to transfer price adjustments by national tax authorities.

Tax incentives used by such tax havens can take the form of zero or low taxation, the absence of withholding taxes as well as differences in the availability of loss carry-forwards or group reliefs.

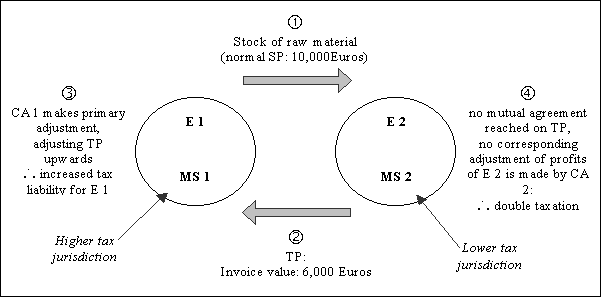

2.3. Case study

A simplified illustration of a transfer pricing situation will elucidate the central matter of this chapter. E1 and E2 are two distinct legal entities forming part of the same MNG of companies. The former is resident in MS MS1 and the latter in MS2. The two enterprises are engaged in commercial and financial transactions between each other and, considering the largely artificial separation between the two enterprises, the conditions of such dealings can easily be manipulated to obtain fiscal benefits for the MNG. A common tax planning opportunity has become evident in that the corporate tax rate obtaining in MS1 is higher than that in MS2. Alternatively, E1 has carryover tax losses which risk not being compensated. Thus the invoice value of a particular transaction or transactions (e.g. the sale of a stock of raw material) is set lower than that which would be charged by independent businesses in similar circumstances. The lower prices paid by E2 should reduce the profits generated by E1 for the purposes of MS1 corporate taxation and therefore a smaller portion of the MNGs profits should be taxed at the higher tax rate applicable in MS1. The correspondingly higher profits generated by E2 should be taxed at the lower tax rate chargeable in MS2, resulting in tax saving for the MNG of companies.

The competent authorities of MS1 are likely to be aware of this transfer pricing opportunity being availed of in this example. The tax administration of MS1 may therefore increase its assessment of the companys taxable profits according to the arms length principle (primary adjustment) and therefore neutralise the tax avoidance scheme for the purposes of E1. However, the tax authorities of MS2 might be in disagreement with MS1 over the adjusted transfer price and may be unwilling to reduce the associated companys declared profits accordingly (corresponding downward adjustment) or they might only be willing to do so following transfer price fixing rules which differ from those applied in MS1. This unilateral adjustment of profits of associated enterprises by national tax authorities causes overlapping assessments of the same income within the Community, which instance of double taxation is precisely what the arbitral procedure contained in the Convention seeks to eliminate.

Figure I. Case study illustrated.

E = Associated Enterprise / Undertaking

MS = Member State

CA = Competent authority

SP = Selling price

TP = Transfer Price

2.4. Authority for transfer pricing adjustments

MSs tax authorities counter transfers of profits or losses by adjusting taxable profits as if transfer transactions were carried out at arms length, thereby re-allocating to the accounts of a taxpaying company the profit which it would unduly have transferred to its associate company using the transfer pricing mechanism.

Typically, the competent authorities derive the power to conduct this exercise from the relative provisions under domestic law. Furthermore, such authority is also found in the bilateral tax treaty, if any, existing between the two countries in question, generally styled in line with the OECD Model:

Where () conditions are made or imposed between the two enterprises in their commercial or financial relations which differ from those which would be made between independent enterprises, then any profits which would, but for those conditions, have accrued to one of the enterprises, but by reason of those conditions, have not so accrued, may be included in the profits of that enterprise and taxed accordingly.

When the relationship between the two enterprises involved in a transfer pricing case is that between an enterprise and its PE, the competent authority derives its mandate from the following provision:

(), where an enterprise of a Contracting State carries on business in the other Contracting State through a permanent establishment the situated therein, there shall in each Contracting State be attributed to that permanent establishment the profits which it might be expected to make if it were a distinct and separate enterprise engaged in the same or similar activities under the same or similar conditions and dealing wholly independently with the enterprise of which it is a permanent establishment.

Of course, the effectiveness of articles 7(2) and 9(1) arises on a specific provision of the domestic tax law of the MS as they are not self executing. Besides, as with most of the countries negotiating entry in the EC, the Contracting States may not have entered any bilateral tax treaty at all. In other jurisdictions, the domestic legal basis for the profit re-instatement is simply derived from the national tax definition of profit.

3. Scope of the Convention

3.1. Personal scope of application

3.1.1. Enterprise of a Contracting State and enterprise

The application of the Parent-Subsidiary and the Merger Directives is limited to enterprises assuming the legal forms listed in the Annexes to the Directives. On the other hand, the personal scope of application of the Convention includes not only the corporate form but also individual persons and partnerships.

In the English version of the Convention, the terms enterprise and undertaking have been used interchangeably. It has been argued that, since the French version uses the term enterprise throughout, it can reasonably be assumed that the two terms should be attributed the same meaning. Nonetheless, the terms enterprise of a Contracting State and enterprise are not defined in the Convention and should assume the meaning given to them by the DTC applicable between the MSs. Where such treaty follows the OECD Model, the definitions are, respectively, an enterprise carried on by a resident of a Contracting State and the carrying on of any business. The term business is in turn taken to include the performance of professional services and of other activities of an independent character.

3.1.2. The connecting factor

The Convention is silent regarding the connecting factor implied between an enterprise and the Contracting State concerned. Referring to the bilateral treaty in terms of Article 3(2) of the Convention, the applicable criterion is residence, which is only defined in terms of the domestic laws of the Contracting Parties. A resident of a Contracting State means any person who, under the laws of that State, is liable to tax therein by reason of his domicile, residence, place of management or any other criterion of a similar nature. In the case of dual residence, also by virtue of Article 3(2) of the Convention, Article 4(2) and (3) of the OECD Model apply and uphold the doctrine of effective management and control as opposed to the incorporation theory.

In the absence of a DTC, domestic law applies (the lex fori). This is not an ideal solution since the incongruous definitions applicable in the Contracting States concerned may result in the inapplicability of the Convention to their transfer pricing cases which were meant to be arbitrable. Similar problems may arise as regards the definition of profits which is nowhere found in the Convention and which is alien to countries such as the UK and Malta (a potential MS). All issues regarding these and other conditions of application of the Convention fall within the jurisdiction of the national court to which the taxpayer would refer his transfer pricing case; they are neither arbitrable under the Convention, nor reviewable by the ECJ.

3.1.3. associated

It is clear that the two (or more) enterprises contemplated by the Convention must be associated as suggested by the heading of Chapter II Section II. This relationship is defined in Article 4(1) (a) and (b) which apply the same criteria used by the ESC to define intra-group transfer pricing, by the 1976 proposed Arbitration Directive to define group of enterprises and by the OECD Commentary to define parent and subsidiary companies and companies under common control. An enterprise and its PE are, by a legal fiction, separate legal entities and this satisfies the prerequisite of association that the two enterprises have to be distinct enterprises for the Convention to apply to them.

3.1.4. Transfer pricing relationships subject to the Convention

The following table shows the number of possible transfer pricing relationships which could potentially be covered by the Convention.

Figure II. Personal-territorial scenarios covered by the Convention

(contact author for figure)

One of the basic conditions for the application of the Convention is the involvement of two enterprises of two different Contracting States. This immediately excludes transfer pricing disputes involving two associated enterprises based in the same MS.

Article 1(1) brings within the scope of the Convention only those enterprises of any Contracting State the profits of which, besides being subject to tax in that MS, also form part, or are likely to form part, of the tax base of other enterprises of other Contracting States (scenario 1 in Figure II). Similarly, by specific provision, the permanent establishment of an enterprise of a Contracting State shall be deemed to be an undertaking of the State in which it is situated. Therefore, the Convention also applies to (a) an enterprise of a MS and its PE in another MS and also to (b) an enterprise of a MS and a PE belonging to an associated enterprise based in the same MS, which PE is situated in another MS (scenarios 3 and 5 respectively in Figure II).

Strictly speaking, basing oneself on Articles 1 and 4, the Convention does not cover the transfer pricing relationship existing between an enterprise of a Contracting State and a PE of an enterprise of a Contracting State which is situated in a third Contracting State. On the other hand, the Joint Declaration to Article 4(1) seems to contradict this result:

The provisions of Article 4(1) shall cover both cases where a transaction is carried out directly between two legally distinct enterprises as well as cases where a transaction is carried out between one of the enterprises and the PE of the other enterprise situated in a third country.

The rather poor drafting and the vagueness of the wording of the Joint Declaration to Article 4(1) as to what is meant by a third country should be so interpreted that it reconciles with Article 1(2) and therefore that the Convention applies where there are two legally distinct enterprises in different Contracting States, with the PE of one of these situated in a third Contracting State (scenarios 6 to 9 in Figure II). It is generally accepted that the Joint Declaration to Article 4(1) should be taken as an expansion or clarification of Article 4(1) rather than a restriction of Article 1(2).

Article 1(2) precludes the application of the Convention to a PE situated within a MS unless the enterprise of which it forms a part is itself an enterprise of a MS. Therefore transfer pricing relationships contemplated in scenarios 10 to 13 and those between PEs based in different MSs, both of which belong to an enterprise based in a non-MS (scenario 14) are not covered by the Convention. Rather than the Convention, the transfer pricing relationship between, say, a US and a German PE of a Swiss corporation would be arbitrable under the US-German DTC.

The MS-based PE of a non-MS-based enterprise would, however, be covered by the OECD Model (Article 9(1)) and secondary adjustments should still be applicable vis–vis the said enterprise as well as the imposition of a withholding tax on a deemed dividend.

3.2. Serious penalty exclusion

Under Article 8, in the case of an enterprise liable to a serious penalty, the competent authority shall not be obliged to initiate the mutual agreement procedure in terms of Article 6, nor to take part in the formation of the advisory commission in terms of Article 7. It can even stop these proceedings.

These serious penalties include not only criminal sanctions but also administrative sanctions. Time will show us whether the concept of serious penalty will be interpreted as widely as to restrict the Convention in serving its preordained purpose. It is however clear that the Convention will definitely apply to associated enterprises which fulfil all their accounting and tax obligations and which are not involved in fraudulent transactions or transactions falling under abuse of law rules.

3.3. Taxes covered

3.3.1. Income taxes

The Convention applies to income taxes generally, in particular, to the number of taxes existing in the Contracting States and listed therein and to any identical or similar taxes which are imposed after the date of signature thereof in addition to, or in place of, existing taxes. Therefore the Convention covers income taxes on physical persons and on companies on residents and on non-residents, principal taxes and surtaxes, present income taxes and identical or similar future income taxes. It does not cover stamp duties, taxes imposed on a taxpayers wealth and other non-profit based taxes.

3.3.2. Other taxes

The wording of the Convention differs from that of the OECD Model in that it remains silent as to income taxes imposed on behalf of political subdivisions or local authorities. The generality of the term taxes on income but then the absence of a mention of these taxes in the list of presently covered taxes are contradictory and ambiguous.

3.3.3. Fines and penalties

Penalties are often calculated as a percentage of the adjusted amounts and make up an integral portion of the adjustment. It is submitted, however, that excessive penalties are prohibited. Article 9 of the OECD Model, running parallel with Article 4, only permits adjustments of transfer prices up to that level independent parties would have remunerated, in accordance with the arms length principle. Ultimately, penalties remain exclusively an internal tax matter of the Contracting States.

3.4. Types of double taxation addressed

The Convention deals with the following types of double taxation:

1. Economic double taxation: which arises when one MS taxes the profits of a subsidiary and these same profits are taxed again by a second MS on payment of dividends to the parent company. The Convention has a specific mandate to eliminate such double taxation suffered by the MNG of companies.

2. Juridical double taxation: which arises when profits, payable to one person, fall within the taxing jurisdiction of two MSs and consequently are taxed twice. A typical instance of juridical double taxation is the scenario of a PE. The profits generated by a branch in one MS form part of the profits of the enterprise located elsewhere to which the branch belongs and are taxed in both MSs. Despite the unitary character of the entities concerned, by specific provision, the Convention considers these as separate and distinct undertakings.

Both forms of double taxation may be the result of transfer pricing adjustments made by multinational enterprises.

3.5. Causes of EC double taxation

In the general considerations of its proposed Convention, the Commission noted that:

() When one countrys tax authority increases the profits of an enterprise but the profits of the associated concern that is its partner in the transaction are not correspondingly reduced in the other country, the group as a whole suffers double taxation.

Such double taxation may well give rise to distortions, both in the conditions of competition and in capital movements, of a kind that would otherwise not exist.

Such consequences are not acceptable within the Community, because they directly affect the operation of the Common Market.

The Convention owes its inception to the above realisation by the Commission. However, how does double taxation arise? First of all, if a network of DTCs links almost all MSs and Article 9 of the OECD Model has been provided, how can double taxation due to transfer pricing arise as in the above case?

3.5.1. Lack of a DTC or of Article 9(2)

The lack of a DTC linking a number of MSs is the first cause of such double taxation. There results a number of such cases and the situation in this respect is likely to be aggravated by the prospective new entrants.

In the case where such bilateral relations have been undertaken, double taxation arises out of the failure by such treaty parties to adopt Article 9(2) of the OECD Model. Whereas Article 9(1) authorises the first treaty party to make the adjustment and neutralise the tax saving scheme, Article 9(2) binds the second State to make corresponding downward adjustments. The absence of this article in a DTC between two States means that such corresponding adjustment is not likely to be made, especially if there are no unilateral domestic provisions to that effect, and the profits in question will form part of the tax base of both taxpayers.

3.5.2. Conflicting interpretations of the arms length principle

For the purpose of the primary adjustment of transfer prices, there exist three main criteria for determining the arms length transfer price applicable between associated enterprises: the Comparable Uncontrolled Price Method, the Resale Price Method and the Cost Plus Method. However, national tax authorities adopt different methods or combinations thereof, thus giving rise to discrepancies and causing double taxation.

3.5.3. Conflicting classification rules for PEs and for company residency

MSs entertain different views on whether a place of business, through which the business of an enterprise is being conducted, should be classified as a PE for tax purposes, and on whether a company should be considered resident in a given MS or not. Consequently, conflicting definitions of PEs and company residency constitute another cause of double taxation.

Under Article 3(2), terms such as permanent establishment and residence, which are not defined in the Convention, shall have the meaning which it has under the DTC between the States concerned. In the absence of a DTC, the applicable interpretation is assumed to be that adopted by Article 5 of the OECD Model.

The OECD Model has not settled the dispute between the taxpayer and the State claiming the right to tax branch profits. It is up to the domestic courts to decide whether a PE has been established and the different appeal stages tend to be quite time-consuming. Similarly time-consuming is determining the conformity of transactions between a permanent establishment of an enterprise and the other enterprise with arms length principles. All this means that it may take years to adjust profits and eliminate double taxation, which raises yet other problems due to some domestic laws which restrict the period in which assessments may be made. The Convention has addressed these timing problems in Article 6(2).

However, the Convention remains silent as to the problem of dual-resident companies and therefore fails to settle the contrasts between the sige rel (real seat) doctrine and the incorporation doctrine embraced by the UK and Denmark.

3.6. Territorial scope

The Convention applies a strictly situs-based (territorial) criterion. It excludes from its scope of application PEs situated in non-MSs, even if they pertain to a EC-based enterprises. It also excludes transfer pricing disputes relating to transactions between two PEs situated in non-Contracting States, even if they belong to enterprises of two MSs.

The territorial scope of the Convention is that laid down in Article 299 (ex-Art. 277) of the Treaty, which defines the territories of the MSs and therefore of the EC. The Convention does not apply to the territories and regions specified in paragraphs 2, 3 and 4 of this Article and to those specified in Article 16(2) of the Convention (certain French territories, the Faroe Islands and Greenland).

This means that the Convention has a narrower scope than the Merger and Parent-subsidiary Directives which apply to all companies resident in the territories and regions covered by the entire Article 299 (ex-Art. 227) of the Treaty. Other conventions concluded on the basis of Article 293 did not exclude such territories and regions.

4. The procedures

Figure III. Overview of procedural steps and their time limits

(Contact author for figure)

5. The unilateral relief procedure

Under Article 5 of the Convention, a Contracting State intending to adjust the profits of an enterprises is bound to inform the enterprise of the intended action in due time. Such enterprise is then given the opportunity to notify the other party to the transfer pricing relationship in question, which in turn is given the opportunity to notify the intended adjustment to the Contracting State in which the latter associated enterprise is based.

While the proposed primary adjustment proceeds unhindered by this passage of information, the two related enterprises and the second Contracting State may, on the basis of this information, agree to the adjustment. Agreement means that the primary adjustment undertaken by the first Contracting State has been unilaterally approved by the second Contracting State which, in the absence of a dispute regarding the application of the principles contained in Article 4, undertakes to make a corresponding adjustment, relieving the enterprises of any double taxation which would otherwise accrue.

Thus, the only requirements imposed by the Convention for the re-allocation to be valid are the first Contracting States duty of notification and that the adjustment must be satisfactory, i.e. acceptable to the tax authority of the second Contracting State and to the associated enterprises in question.

Before and during this phase of the operation of the Convention, according to the interpretation of Article 5, the tax authorities are free not only to go ahead with the adjustment but also to assess and collect the additional taxes due. Of course, the domestic laws of the Contracting State may allow a stay of the assessment proceedings or at least a stay of the enforcement of an assessment, but this is entirely a domestic tax affair. The ESC believed that the 1976 Draft Directive should require a deferment of the collection of the additional tax so as to give the competent authority making the adjustment an incentive to conduct negotiations as expeditiously as possible.

6. The mutual agreement procedure

Article 6 of the Convention provides in the first place for a mutual agreement procedure which is very similar to the procedures set up by bilateral tax treaties. Under this procedure, the competent authorities of the two Contracting States are to seek a solution of the transfer pricing dispute by mutual agreement. However, they are under no obligation to actually reach such an agreement.

6.1. Initiation of the international procedure

In the event that no agreement is reached, the international procedure is set in motion on an administrative level. In terms of Article 6, where an enterprise considers that the principles set out in Article 4 have not been observed, it may, irrespective of the remedies provided by the domestic law of the Contracting State concerned, present its case to the competent authority of the Contracting State of which it is an enterprises or in which its permanent establishment is situated. The case must be presented within three years of the first notification of the action which results or is likely to result in double taxation within the meaning of Article 1.

As the above wording suggests, the initiative of submission lies not in the hands of the competent authorities but in those of the victims of double taxation, the associated enterprises. This Article excludes the initiation of the mutual agreement procedure in cases not contemplated by the Convention and in cases which are undisputed in terms of Article 5; these cases can only be dealt with in foro domestico.

The form of submission for the international procedure is not regulated by the Convention but it has been suggested that the form of filing a domestic tax complain should be applied, e.g. by registered post, setting out the reasons for the complaint (involving a breach of the principles of Article 4) and the resulting or potential double taxation. Also, unless the competent authorities would have agreed on a common rule of conduct for the issue, domestic rules apply as to whether the submission should be accompanied by the arguments and backing documentation or whether these should follow at a later stage.

6.2. Other Contracting States concerned

The affected enterprise should at the same time inform its authority of any third and other Contracting States which could be concerned and the said authority should then without delay notify the competent authorities of those Contracting States. It is advisable to effect a protective notification about other states which could possibly become involved.

6.3. Three-year term for complaint

The complaint must be presented within three years of the first notification. The three year period sets aside the shorter two year time limit applicable to the mutual agreement procedure under some bilateral treaties between Contracting States. The said term starts running from the first notice (in terms of Article 5) of the threatened adjustment which would result in a second assessment of the profit transfer.

6.4. Procedural rules of conduct

The negotiations between the Contracting States are essentially diplomatic and these will themselves determine the procedural rules for the conduct of such negotiations. The Convention does not impose any such rules. Moreover, the legal position of the affected taxpayer is not recognised as the latter and its competent national tax court are not bound by the Convention.

6.5. Time-limit for mutual agreement

Contracting States are allowed to secure a solution by mutual agreement during a period of two years commencing on the date on which the case was first submitted to one of the competent authorities in accordance with Article 6(1). This is considerably shorter than the term applicable under the mutual agreement procedure contemplated in bilateral DTCs, which may last as long as ten years.

However, there are two ways of looking at this. Hinnekens argues that the competent authorities, aware of the final say of the arbitration commission looking over their shoulders, may let this period expire without active and complete examination of the case. On the other hand, other tax lawyers argue that the competent authorities will tend to utilise this term well so as to decide themselves the applicable solution, rather than leave it in the hands of the arbitral commission.

6.6. Domestic v. international proceedings

The case is referred to and settled by international procedures, irrespective of the remedies provided by the domestic laws of the Contracting States concerned. The domestic and international procedures are not mutually exclusive and do not compete as the mutual agreement is only binding on the Contracting States and not on the national courts. The affected taxpayer is therefore placed in a tactical position, facing optional parallel proceedings. An enterprise can choose one or the other, or a combination of both. In the latter case, the enterprise can choose to call for the discontinuation of the international procedure if it is satisfied with the elimination of double taxation afforded by a decision of the national courts.

7. The arbitration procedure

7.1. Procedure and composition of the advisory commission

If the mutual agreement procedure yields no results within two years of the case being presented, the competent authorities must set up an advisory commission to deliver an opinion on the elimination of double taxation.

If more than one competent authority is involved, the procedure may be conducted as a single multilateral arbitration in which the competent authorities of the enterprises concerned participate simultaneously. In the more complex cases, this option is preferable to separate procedures, as the latter, done on a piece-meal basis, tend to produce results which are inconsistent or incoherent in the multilateral context.

Each advisory commission comprises two representatives of each competent authority and an even number of independent persons to be appointed by mutual agreement or by ballot by the competent authorities, and these representatives and independent persons shall jointly elect a chairman from a list of independent persons. There is an uneven number of members of the commission and the majority decision is likely to depend on the votes of the independent members if the representatives of the two competent authorities should not be able to reach an agreement.

The commission must deliver its opinion within six months and such opinion shall be adopted by a simple majority of its members. Where an enterprise pursues a remedy before a domestic court or tribunal, the two years within which the competent authorities have to reach agreement run from the date of judgment of the final court of appeal. Also, the submission of the case to the advisory commission shall not prevent a Contracting State from initiating or continuing judicial proceedings or proceedings for administrative penalties in relation to the same matters.

If, within a further six months, agree cannot be reached on alternative steps to eliminate double taxation, the competent authorities must accept the commissions decision.

7.2. Legal nature and consequences

There are two schools of thought regarding the legal nature of the commission procedure and decision under the Convention, as follows.

7.2.1. An administrative act

Some maintain that the mechanism contemplated in Articles 7 to 11 is meant to address the absence of an obligation to reach an agreement which characterises existing bilateral DTCs without going as far as creating an arbitration procedure which would deprive Member States of their sovereignty over tax matters.

Thus, according to the proponents of this theory, the final decision to settle under the Convention remains in the hands of the Contracting States involved and the commission mechanism merely forces the Contracting States to come to a mutual agreement and eliminate an instance of double taxation in a way chosen by common consent. Under Article 12, they are free to take a decision which deviates from the advisory commissions opinion and only if they fail to agree are they obliged to adopt the commissions opinion.

Moreover, the terminology adopted by the Convention seems to reinforce this view (advisory and opinion) as does the two-step system leaving the decision formally with the competent authorities. One can be lead to conclude that the legal nature of the procedure is not a jurisdictional act and that the decision is not taken by a supranational arbitral body but by the Contracting States.

Furthermore, the changes in legal form from a directive to the present Convention, forfeiting in the process such characteristics as the express terminology indicating arbitration (arbitration, decision) and the outright arbitral procedure, constituted a refusal of the Contracting States to accept the entailed incursion on their sovereign jurisdictional rights.

Thus, the commission procedure is an intergovernmental, and therefore diplomatic, agreement of a purely administrative nature and therefore its opinion is not binding on the Courts of the Contracting States.

7.2.2. A jurisdictional act

By way of counter-argument, it is submitted that a number of factors demonstrate that the Convention is indeed about arbitration and that it does involve the partial surrender of the Contracting States fiscal sovereignty, even if, and this is not disputed, the Contracting States intention was to minimise the forfeiture of a degree of their fiscal sovereignty.

The commissions opinion is, even if indirectly, not only potentially binding, but very likely to be so. It is argued that if two Contracting States were not able to agree on a solution at mutual agreement stage, it is highly unlikely that they would agree differently once an arbitral decision has been pronounced the vantage point of the party winning the arbitration is such that it would not be in this partys interest to seek such alternative. So likely is it that the opinion will be binding, that the Convention uses the terms opinion and decision interchangeably and, even if exceptionally, also the term arbitration procedure (heading of Chapter II, Section II).

We find other factors backing this reasoning: the rules on the composition of the commissions, the qualifications and secrecy obligations of their members, the institutional framework and own procedural rules as well as the recognition of taxpayers rights. All these transform the commission into a truly arbitral body, separate from the Contracting States, and its opinions into truly jurisdictional and supranational decisions.

It follows therefore that the affected enterprises can only bring before its national court cases of Contracting States failure to fulfil their obligation. A dilemma concerning cases for the enforcement of an arbitral award is that the national courts will have the choice of enforcing either the award or a different bilateral transfer pricing ruling on the same transaction, to which the competent authorities would have agreed earlier on and which would be binding on them. The only determinative and available solution for the Court is to uphold the award.

7.3. Appeals issue

7.3.1. Appeals in domestic courts

Ones approach to the question of whether an appeal is possible from the solution resulting after the four-stage process introduced by the Convention is determined by whether one forms part of one or the other of the above schools of thought.

The advocates for the administrative nature of these procedures conclude that, being simply a decision agreed to between the administrative authorities of the Contracting States, such decision should be appealable before the domestic courts. This also applies to agreements between Contracting States under the mutual agreement procedure applicable under their bilateral DTCs.

The proponents of the alternative doctrine maintain that the commissions decision is jurisdictional in nature and the commissions authority supranational and therefore, such decisions do not admit of appeals in foro domestico. However, is it possible to have an international review of the arbitral decisions?

7.3.2. Appeals in the international domain

Such a possibility can be interpreted of Article 13 which lays down that the fact that the decisions taken by the Contracting States have become final shall not prevent recourse to the mutual agreement procedure and the arbitration procedure afresh. Some authors have interpreted this to imply the possibility of enterprises to start over the international procedure if they believe that the decision taken by the Contracting States does not comply with the Conventions principles or that the decision did not consider facts which happened subsequently. Even if this view should be upheld, the time limits laid down by the Convention will not start running afresh and therefore, taxpayers will be able to re-open international procedures, subject to the three year time limit imposed by Article 6(1).

In a democratic society, it is expected that the post-award controls incorporated in the 1950 European Convention for the Protection of Human Rights, in the 1981 International Covenant on Civil and Political Rights and in the 1958 Convention on the Recognition and Enforcement of Foreign Arbitral Awards should form part of the taxpayers rights under the Convention and that therefore, the final decision imposed by the Convention should be subject to appeal also on the basis of these treaties.

7.4. The nature of the final decision

The commissions decision is only potentially binding as its binding force is conditional to the competent authorities, within a further six months, failing to reach an alternative solution to the dispute. The authority of the advisory commission, therefore, is limited to submitting an opinion containing a decision capable of being implemented by the tax authorities if these should fail to reach an agreement.. It is up to competent authorities to act by common consent on the basis of Article 4 and take the final decision which has to eliminate the double taxation. They may deviate from the opinion rendered by the advisory commission or allow the commissions opinion to become binding.

Whichever of the two options is chosen, the double taxation of profits shall be regarded as eliminated if the profits are included in the computation of taxable profits in one State only; or the tax imposed on those profits in one State is reduced by an amount equal to the tax payable on them in the other State. The solution will depend on whether the Contracting States adhere to the exemption method or the tax credit method. Cases where the right to tax an item of income is divided between the two States would be incompatible with the exemption method. The Convention fails to address cases where one or both of the enterprises incur a loss even though they are expressly targeted by Article 1(3).

According to Killius, where a loss carry-forward is available, a reduction of a loss as a result of the re-allocation of income will just defer the incidence of double taxation. Conversely, if a loss carry-back is available, a lower amount of tax paid in previous years would be refundable. These problems may be aggravated under imputation systems or where other tax credits may be available. None of these aspects are specifically addressed in the Convention.