Taxation of e-commerce:

The Challenge of E-commerce to the Definition of a Permanent Establishment:

The OECDs Response

2002 Dr Jean-Philippe Chetcuti. All Rights Reserved.

Table of Contents

1. Introduction

Electronic commerce – a definition

Electronic commerce comprises the electronic sale by online stores of downloadable soft merchandise such as music, e-books, e-newsletters, photos and video recordings, software and documents (direct e-commerce), the electronic ordering of tangible products (indirect e-commerce), online securities transactions as well as the provision of financial or other services. It also includes the subscription to and use of an internet service provider (ISP) or an online service provider (OSP), and has also been held to cover electronic data interchange (EDI), electronic fund transfers (EFT) and all credit and debit card activity. E-commerce transactions can be business-to-business (B2B) or business-to-consumer (B2C).

The fundamental characteristic of e-commerce, which distinguishes it from traditional commercial activity, is that it is conducted by electronic means. Thus, the marketing of products or services is carried out through the enterprises web site; customers browse online catalogues and use secure online-shopping cart systems; orders are made via interactive online order forms; payment is effected by credit card via secure payment systems; and delivery is either arranged by traditional means (mail, shipment, etc.) or alternatively by allowing the downloading of digitalised products from the web site onto the consumers computer.

The characteristics of e-commerce

E-commerce is characterised by the following features. It is:

![]() Potentially virtual the presence of an enterprise in another country may be wholly based on the hosting of a web-site on a server located there.

Potentially virtual the presence of an enterprise in another country may be wholly based on the hosting of a web-site on a server located there.

![]() Disintermediated and less labour intensive the main enterprise no longer requires intermediaries in foreign countries to be able to conduct business there. Moreover, e-business activities require far less human intervention, if any, than that otherwise required to trade by in a traditional manner.

Disintermediated and less labour intensive the main enterprise no longer requires intermediaries in foreign countries to be able to conduct business there. Moreover, e-business activities require far less human intervention, if any, than that otherwise required to trade by in a traditional manner.

![]() Global the scope of market-penetration is unlimited and knows no borders;

Global the scope of market-penetration is unlimited and knows no borders;

![]() Anonymous business is transacted on a non-face to face basis and therefore the seller and the consumer may not know each other.

Anonymous business is transacted on a non-face to face basis and therefore the seller and the consumer may not know each other.

These same advantages, which have revolutionised the way commerce is conducted, now present fiscal and other legal difficulties which were inexistent under the pre-internet legal order. Never has a technological innovation or invention ever challenged the worlds economic and legal foundations so drastically. It comes as no surprise that the tax impact of e-commerce has been dubbed the most consequential tax issue of the new millennium.

The concept of Permanent Establishment

The tax treatment of cross-border commerce is the subject of bilateral tax treaties which are often negotiated versions of the OECD Model Tax Convention. According to Article 7 of OECD Model, the source country may tax the profits arising from commercial activity carried out within its borders by a foreign entity through a substantial physical presence in the source country. To justify source taxation, such presence must reach the level of a permanent establishment by satisfying the following three prerequisites, namely that there must be a distinct place, such as premises, or in certain instances, machinery or equipment (place-of-business test), that this must be established with a certain degree of permanence (permanence test), and that business must be carried on through the place, usually by personnel of the enterprise (business-activities test).

If the presence does not reach the level required by the OECD Model by satisfying these requirements, the source state is not entitled to charge income tax on the profits arising from the international transaction; rather, the residence country will have the right to tax the profits of its resident.

The requirement of a PE in source countries is comparable to the US substantial physical presence test. Constitutionally, in the US, a state is entitled to impose state and local sales taxes an enterprise of another US state only if such business maintains a substantial physical presence within the former state.

Policy considerations – the rational behind the PE principle

Historically, the concept of PE answered the internationally-felt need for a quantitative criterion for ascertaining the taxability or otherwise of foreign commercial activity in the source state. The PE principle provided sufficient evidence that a foreign companys business within the source country was substantial enough to justify the imposition of fiscal compliance burdens on the foreign company in that country.

This concept satisfied the requirement of certainty and predictability of tax law in that it provided multinational companies with relatively clear rules to determine in advance whether and in what way their activities abroad would be taxed by foreign tax authorities. Furthermore, the PE principle presented states with an internationally equitable rule for sharing the benefits of cross-border commerce source country taxation rewards importing countries for opening to foreign businesses the commercial opportunities available within their markets, while net-exporting countries obviously reap the benefits of taxing value added at the production stage.

2. The Challenge of E-commerce

With the advent of the Digital Age, the international tax community saw the PE concept face its first major challenge. With the dotcom boom at its peak, e-tailing ventures selling digitalised products appeared, tapping into the global online market and capitalising on the lower overheads associated with on-line trading.

Disintermediation

Removal of Physical Intermediaries and consolidation

Traditionally, multinational corporations have sought to penetrate foreign markets by setting up physical intermediaries within the targeted markets. For instance, retailers have carried out their marketing campaigns via sales offices operating in the foreign market. These physical intermediaries often constituted PEs under tax treaties, triggering source-based taxation.

The picture changes with the availability of e-commerce opportunities. E-tailers such as Amazon.com effect the greater part of their market research, advertising, marketing and sales through a web site. This increases competitiveness, transferring transaction costs, including product selection, to customers so that the cost-savings for the online retailer is tremendous. Thus, the Internet can be seen as an agent of disintermediation because it removes the necessity for certain intermediaries. Even stockbrokers have felt the pinch of online competition. E*trade.com permits retail stock trading without brokers, along with Charles Schwab, Datek Online, CyberInvest.com, Ameritrade, Inc., 5Paisa.com and a multitude of other e-brokers now in the trade.

For the multinational corporation, disintermediation means shifting part of their business operations from their physical intermediaries in source countries to their e-commerce base in the country of residence, thereby centralising their administrative, sales, marketing and after-sales operations and outsource non-essential functions to foreign affiliates. For source countries, this means a loss of source-generated taxable profits and, as long as international tax rules insist on the physical presence requirement, their tax base will suffer further erosion.

Removal of Human Intermediaries

The latest internet technologies can now also perform those tasks traditionally carried out in source countries by dependent agents or employees employed by multinationals. Complex contracts can be concluded remotely and new business relationships created online. The processes of order collection, contract negotiation and payment collection can now be automated. The removal of dependent agents habitually concluding contracts in the source state means that a PE may no longer be present under most tax treaties. The same result can be achieved by replacing dependent agents with independent agents acting on instructions to perform the same tasks. Meanwhile, customer relationships are maintained via the companys intranet. Under the current international tax regime, no tax can be chargeable by the source state for the corporations activities in its market.

Reintermediation and the cybermediary

New opportunities are created especially in the B2B sector for the role of the cybermediary, an online company engaged in facilitating business transactions online, without having fixed places of business within source countries. Online infomediaries, like Vertacross.com and Ariba.com operating in the e-procurement business bring buyers and sellers together on the Internet, greatly reducing transaction costs for both parties. These new intermediaries are performing operations outsourced to them by multinational corporations.

With more and more businesses going virtual and with a greater portion of source state activity carried out without a PE, source states are justified to fear that their tax legal entitlement to tax foreign activities within their markets is steadily being curtailed. Furthermore, the anonymity of internet transactions means that internet activity is difficult to trace; residence states tax authorities too could lose their ability to detect taxable business activity. E-commerce ventures would be able to elude fiscal liability altogether.

Web Sites and Servers

With the destabilisation of the traditional concept of PE, attention has quickly shifted onto servers and web sites for their possible qualification as a PE. Can a server, telecommunications device (such as a cable used in transmission), computer terminal, or web page be considered a PE?

A web site of an e-commerce business is a combination of software and electronic data stored on and operated by a server.

Others have described a web site as a companys or an individuals collected web documents. It is clear from these two definitions that a web site is intangible and as such cannot alone make up a place of business. To satisfy the latter requisite, there has to be a facility such as premises or, in certain circumstances, machinery or equipment.

An internet server consists of tangible computer equipment networked to the internet. A server is usually dedicated to the storage and internet accessibility of web sites, email accounts and databases and software programmes resident on the server can automatically administer the electronic transmission of digitalised e-commerce products or services to end consumers. E-commerce ventures may use the web hosting services of ISPs who allocate and make available to them sufficient server space for their e-commerce requirements. Alternatively, such firms may own or lease a server so as to command a higher level of control over the server.

Typical e-commerce models

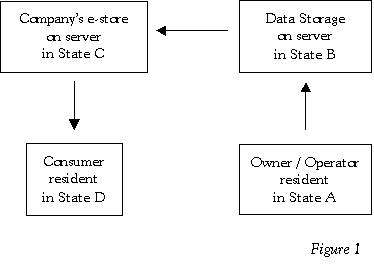

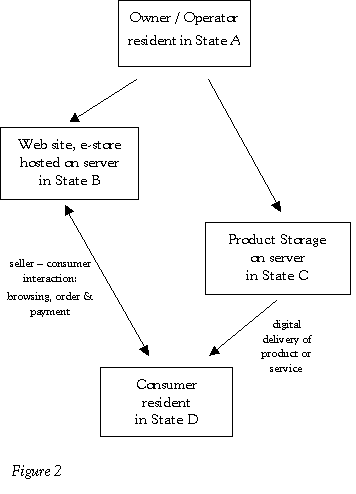

Typically, foreign e-commerce operations are carried out by means of servers located in the target markets. Dotcom ventures can adopt various working models or server combinations. An e-commerce transaction can involve a number of servers strategically located in different countries. The firms web site and its online store can be hosted on different servers or on one and the same server situated anywhere in the world and accessible by online consumers from any part of the world. For the downloading of the soft merchandise purchased from the e-store, the web site then retrieves the data from a server elsewhere on which the data is stored and sends it electronically to the customer (refer to Figure 1 supra). Alternatively, the consumer is (either voluntarily or unknowingly) redirected to another server which holds the firms data (refer to Figure 2). Tax planning reasons apart, servers are usually so located so as to optimise the downloading process of soft merchandise onto purchasers disks.

Typically, foreign e-commerce operations are carried out by means of servers located in the target markets. Dotcom ventures can adopt various working models or server combinations. An e-commerce transaction can involve a number of servers strategically located in different countries. The firms web site and its online store can be hosted on different servers or on one and the same server situated anywhere in the world and accessible by online consumers from any part of the world. For the downloading of the soft merchandise purchased from the e-store, the web site then retrieves the data from a server elsewhere on which the data is stored and sends it electronically to the customer (refer to Figure 1 supra). Alternatively, the consumer is (either voluntarily or unknowingly) redirected to another server which holds the firms data (refer to Figure 2). Tax planning reasons apart, servers are usually so located so as to optimise the downloading process of soft merchandise onto purchasers disks.

The (in-)applicability of traditional PE-based taxation

According to Prof. Hinnekens, the fundamental distinctions and categories that previously guided traditional international tax law have been blurred by this relatively recent phenomenon. Hinnekens doubts whether tomorrows business may be effectively taxed under application of yesterdays rules. Thus, the geographical categories of PE and residence for tax purposes now face renewed challenges, as do the distinctions between preparatory services and core activities, between goods and services, between services transactions and property transactions, and so on.

According to Prof. Hinnekens, the fundamental distinctions and categories that previously guided traditional international tax law have been blurred by this relatively recent phenomenon. Hinnekens doubts whether tomorrows business may be effectively taxed under application of yesterdays rules. Thus, the geographical categories of PE and residence for tax purposes now face renewed challenges, as do the distinctions between preparatory services and core activities, between goods and services, between services transactions and property transactions, and so on.

Moreover, the application and enforcement of traditional tax rules is more difficult in cyberspace than in the brick-and-mortar business world. Events which would normally give rise to tax liability in the latter world are likely to escape detection by fiscal authorities in the electronic world and unintentional non-taxation would result. Dotcoms can potentially exploit these new business avenues to gain a competitive tax advantage over their traditional competitors. It is therefore evident that governments worldwide must react to this new threat to their fiscal effectiveness.

3. The OECDs Reaction

The 1998 OECD Ministerial Conference of Ottawa

OECD confirmed leading role in taxation and e-commerce

The 1998 OECD Ministerial Conference confirmed the OECDs mandate, first proposed in November 1997, to assume the international leadership in coordinating the work on electronic commerce and taxation. The OECD and the European Union would co-operate on consumption tax issues while the World Trade Organisation and the World Customs Organisation would concentrate on tariff issues and on customs issues respectively.

The application of existing tax rules to e-commerce

This preference for traditional principles relies on the view that radical changes to the international tax system are unwarranted because e-commerce simply places pressure on existing problems, such as international transfer pricing.

All the twenty-nine OECD MSs, including the US , represented at the Ottawa Conference agreed with the Committee on Fiscal Affairs recommendations that [t]he taxation framework for electronic commerce should be guided by the same taxation principles that guide governments in relation to conventional commerce. Any new administrative measures should be directed toward the application of existing taxation principles and should not be intended to impose a discriminatory tax treatment on e-commerce at this stage of development in the technological and commercial environment. Likewise, it was agreed that the canons of taxation generally applicable to taxation of conventional commerce should equally apply to e-commerce, namely: neutrality, efficiency, certainty, simplicity, effectiveness, fairness, and flexibility.

It was agreed that five Technical Advisory Groups should be created to implement the CFAs recommendations. These included individuals from the industry and representatives from OECD member and non-MSs. Moreover, several OECD Working Parties were formed to produce reports and discussion papers on various e-commerce tax issues.

Implications for net e-commerce importing and exporting countries

Most OECD MSs endorse the view that servers can constitute PEs in some circumstances, while acknowledging the importance of a fair sharing of the tax base internationally. Net e-commerce importers facing the prospect of losing their grip on taxable PEs, are actively pursuing consensus on mechanisms which serve to protect their tax base, such as the taxability of servers as PEs under existing international tax principles. Alternatively, in the (re-)negotiating stages of bilateral tax treaties, net importing countries may be willing to give up server/PE criteria in exchange for other tax concessions granted by net exporting countries.

Clarification on the Application of the PE Definition in E-Commerce

The Draft Commentary on Article 5 concerning the application of the current definition of PE the context of e-commerce, issued by Working Party No. 1 on Tax Conventions and Related Questions, was adopted by the CFA on 22 December 2000.

Web sites and servers

The approved changes to the commentary on Article 5 distinguish between web sites and servers for PE purposes so that web sites stored on a server should not constitute a PE. On the other hand, the server on which the web site is stored and through which it is accessible is a piece of equipment having a physical location. Such a location may constitute a fixed place of business of the enterprise that operates that server as long as the server is fixed at a certain place for a sufficient period of time. The permanence test looks at whether the server has actually been moved, irrespective of whether it can or cannot be moved.

A distinction is also made between the web site operator and the server operator, who may or may not be the same person. The former enterprise carries on business through the web site but does not necessarily operate the server. In the case of web hosting arrangements, the enterprises web site is hosted on a server operated by an ISP. A PE may only arise where the server is at the disposal of the online enterprise who owns or leases it, and can never arise in the case of ISP hosting.

ISPs, web sites and agency

Paragraph 42.10 makes it clear that ISPs cannot constitute dependent agents because they do not have authority to conclude contracts in the name of the enterprise, because they do not do so regularly or because they constitute independent agents acting in the ordinary course of their business, as evidenced by the fact that they host the web sites of many different businesses. Neither can a web site constitute a dependent agent as it is not itself a person in the sense of Article 3 of the OECD Model.

Core functions

However, this requires that the functions performed at that place be significant as well as an essential or core part of the business activity of the enterprise:

Where [the server] functions form in themselves an essential and significant part of the business activity of the enterprise as a whole, or where other core functions of the enterprise are carried on through the computer equipment there would be a permanent establishment.

The new additions to the Commentary on Article 5 provide an indicative list of examples of core functions in the case of e-tailers. These depend on the nature of the business carried on by the enterprise and need not all occur in any given case: the conclusion of the contract with the customer, the processing of the payment and the delivery of the products, all of which are performed automatically online.

Preparatory or auxiliary activities

An indicative list of activities generally considered preparatory or auxiliary includes providing a communications link, advertising goods or services, relaying information through a mirror server, gathering market data or supplying information. Whether these or other server activities should be characterised as auxiliary or preparatory in nature needs to be examined on a case-by-case basis having regard to the various functions performed by the enterprise through that equipment. Thus online advertising, the provision of an online catalogue or the provision online of information to prospective customers by an e-tailer does not create a PE. On the other hand, an online advertising agencys online adverts or the online research activities of an online market analyst are likely to constitute core activities and this contribute to establishing a PE.

Human intervention

The new Commentary also indicates that servers can constitute PEs even if no on-site human intervention is involved or necessary, in the same way as automatic pumping equipment used in the exploitation of natural resources can make up a PE. The CFAs decision to allow the taxation of business profits generated by servers seems to have precedent. By analogy, servers may be compared to automatic equipment such as vending and gaming machines which thought to suffice for the purpose of a PE. On the other hand, it is not unknown for tax treaties to contemplate fictions which favour source country taxation despite the absence of any real PE, as in the case of foreign athletes or artists generating earnings without a PE. Such precedents support arguments that source countries should tax e-commerce profits from sales within their jurisdictions even in the absence of a PE.

Summary of requirements for a Server-PE

For a server to constitute a permanent establishment, it has to meet the following requirements:

1. The server on which web site is hosted and its location have to be at the foreign enterprises disposal owned / leased and operated by the enterprise not web hosting;

2. The server must be is located in the taxing state a fixed place of business;

3. Core business activities have to be performed through the server, as opposed to preparatory or auxiliary functions, without the need for human intervention.

4. Conclusion: Problems solved?

The problems posed by the technology of the New Economy seem insurmountable. It is debatable whether the OECDs clarification of the definition of a PE has helped restore the equitable sharing of tax revenues between residence and source countries, and this for a number of reasons.

Servers are highly mobile and flexible in nature. A server need not have any geographic connection either to the source country or to the residence country. Therefore e-businesses may own or lease a server located anywhere in the world and can conduct its business activities via this server in such a way as to ensure that their profits will either be taxed exclusively by the residence country or by some low tax jurisdiction. Moreover, servers can transfer their programs almost instantaneously to a server in a different jurisdiction as necessary. Furthermore, the server can be maintained or programmed remotely by employees located outside of the source country or serviced by experts in the server state.

A flaw of the OECDs position is that it ignores the possibility of e-commerce functions being transferred to the end consumers computer. Web servers often plant small programs or applets in the users computer which then performs a portion of the processing itself. Alternatively, e-commerce functions can be decentralised via peer-to-peer networking where users trade digital products without resorting to any centralised server location. All these possibilities render the task of determining the location of a PE very difficult, if not impossible. Ultimately, networking technologies have created a breading ground for tax planning opportunities which encourage the relocation of servers across borders. The current PE rules can easily be circumvented either by carrying on only preparatory or auxiliary activities in the source state, or by using the server of a local ISP to carry on the core business activities of the foreign enterprise, or by positioning the server and establishing a PE in low or no tax jurisdictions. Similarly, domestic vendors too can very easily create a PE in lower tax jurisdictions elsewhere.

Another problematic matter is that of enforcement and administration. How can tax authorities determine the income attributable to software functions within servers, to a server or web site? How about the significant compliance costs that could burden multinational businesses having to comply with fiscal obligations in every jurisdiction where their servers are located? These are the questions that face the international fiscal order in the years to come. Meanwhile, efforts by regulators to transpose conventional international tax principles into the virtual world seem to be failing.